- First Name

- Jay

- Joined

- Oct 1, 2019

- Threads

- 39

- Messages

- 2,123

- Reaction score

- 9,864

- Location

- Granger,IA

- Website

- www.grangerford.com

- Vehicle(s)

- *

- Your Bronco Model

- Badlands

Gotcha. Yeah, anything under $700 per month is a normal financed car note for 60 month loans, milage varies.Nope never put anything down on a lease. Thats stupid for other reasons. I always roll in the down payment into the monthly, and pay the bare minimum to walk out the door.

My problem is that im so accustomed to leasing 40-50k cars for 350/mo (under REALLY well negotiated lease deals - nothing down but tax and title). And steer very clear away from brands that dont lease well.

Which is why i want my payments low. But i suppose my options are big down payment. Or typical down payment, and in a year, if there are no bugs i could refi into a lesser loan amount to lower my payments....and if for whatever reason rates are horrendous, I'll wait a year for no bugs and if there are no better refi opportunities, then i would just pay off the entire car in the following year or two (which im not opposed to if rates are 4-5+%).

Although my neighbor recently bought a wrangler in cash and the thing was out of commission for 6+ months for a problem jeep gave him a hard time fixing under warranty. Fixed now, but Im sure his advice would be DONT DO IT.

Based on low auto rates (2-3%), i would highly recommend against significant down payments on any vehicle. I know it feels better to have a lower payment, but making an extra payment each year significantly cuts into the already low interest costs and keeping funds in your account is much safer in case emergencies arise. This will be the first car I purchase that exceeds the $500 payment myself (I don’t normally spend big $ on cars), but if it’s something you love and will take care of, it’ll be worth it.So I have always leased my cars. I dont think this will lease well, so i will buy.

My income is very much split between lump sum annual bonus/commission, and a base salary. I really like the idea of having low payments through out the year for real-feel cash flow, and it's less sweat to make a big payment once a year.

That said, i really want to keep payments at exactly $500/mo, and will front load a down payment. I was thinking of maxing out Ford 1.9% APR @ 72 months, and then putting whatever down to back into $500/mo. I dont have a trade-in, since all my other cars are leased. After doing the math is looks like around a $20k down payment (inc tax, fees, etc) for my build.

Given the low rates, could i put my down payment money aside and use it towards the bigger bills? sure. But mentally, i just do not want to look at a ~$800 bill every month.

Does that sounds like the right approach? I am a bit weary of tying up all that money in the off chance my model Year 1 car has flaws, or is potentially a lemon....and i have to wait to get my money back, versus just returning the car....Another idea is to put less of a down payment, then wait a year to see if any major problems arise, then I could make a big lump sum payment to get my payments adjusted down to $500/mo. So my question in that situation is - will Ford adjust down my monthly payment, or will they just shorten up the term and keep my payments the same?

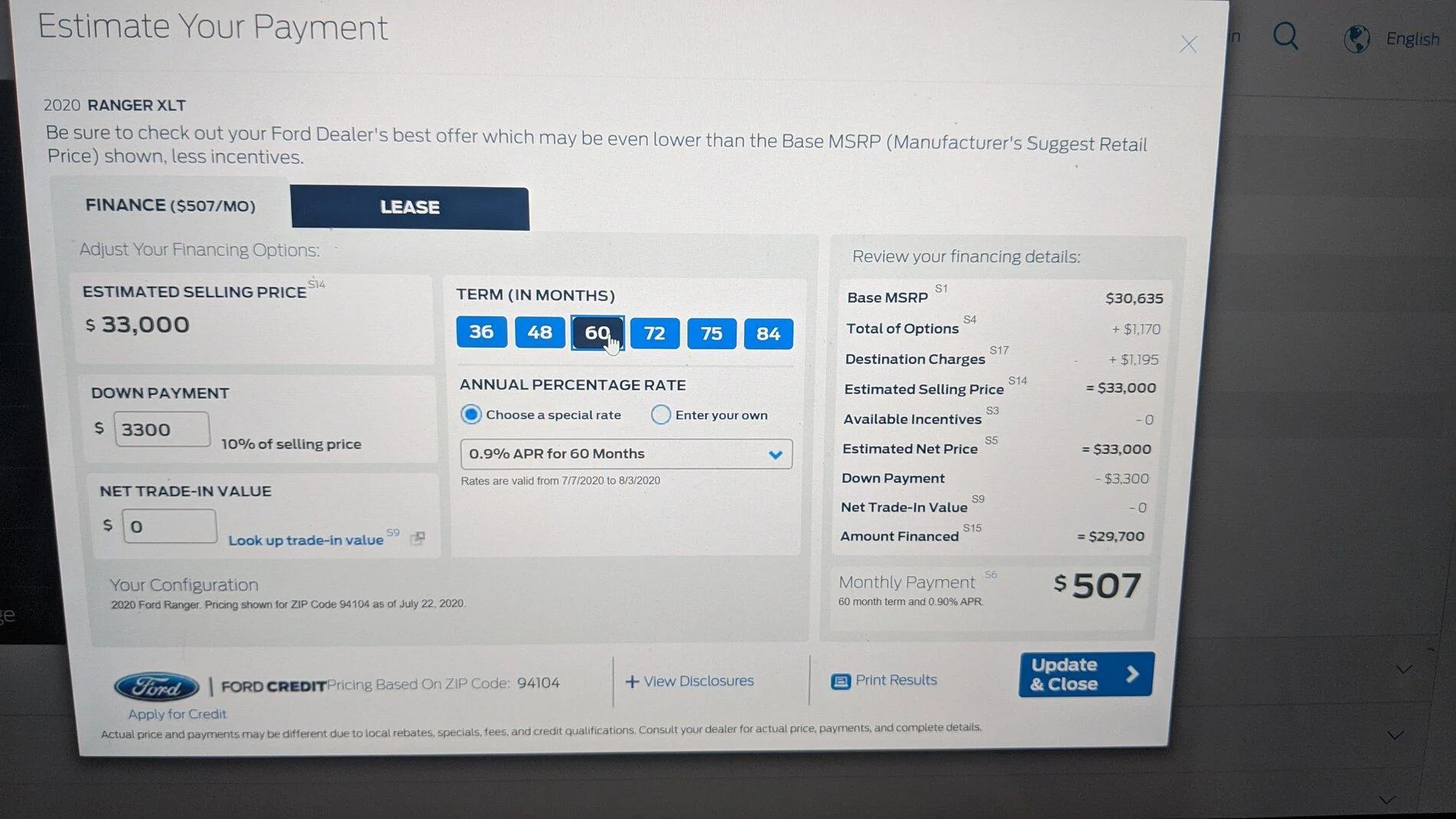

36 and 48mo are 0%, 72 months was 2.9Can you send a link to something that shows that Ford offers 1.9% on any vehicle.

what’s the credit criteria for fords 1.9% financing?I saw a few articles describing their current financing. They have a new flex financing concept that a lot of ppl are reviewing (and bashing it) and comparing / recommending to go for their current 1.9% offered for 60 or 72 mos

Nope... You'll just come to the end of the term sooner....We have plenty saved. 20k in a car doesn’t put us at any risk. Putting personal finances aside -

Question is moreso am I thinking about this right? And will Ford lower my monthly if a make a big lump sum in Year 2?

I got 0% for 72 months last year on my Escape.Can you send a link to something that shows that Ford offers 1.9% on any vehicle.