- Thread starter

- #1

Just passed my 3 year mark in December and looking to get a lower rate. I financed in 2021 when rates were crap. Where did you refinance and what was your rate?

Sponsored

This. First thing you should do is call whoever it's currently through and ask if they will lower it. Let them know otherwise you will refinance and go with someone else. You literally have nothing to lose.Call your lender and ask if they have any better options or try a credit union (if not already)

When you do this, allude to the fact without saying it that you are concerned about and want to be sure you can continue to make the payment.This. First thing you should do is call whoever it's currently through and ask if they will lower it. Let them know otherwise you will refinance and go with someone else. You literally have nothing to lose.

Call your lender and ask if they have any better options or try a credit union (if not already)

Out of curiosity how bad is your current rate?I financed through Ford. I heard that they will not give you a lower rate.

6.75% and that was with an 820 credit score.Out of curiosity how bad is your current rate?

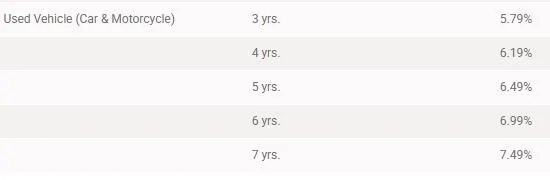

When I look at the credit union I financed through, their used rates are as follows:

And those rates are 1% higher than their typical new car rate. None of those seem appealing to me.

The main issue you are going to run into is that your vehicle is too old to qualify for new car rates and used car rates are always higher, so you're likely to end up with a rate that's no better than what you have now, unless your credit substantially improved and you had a bad rate (for the time).Just passed my 3 year mark in December and looking to get a lower rate. I financed in 2021 when rates were crap. Where did you refinance and what was your rate?

The main issue you are going to run into is that your vehicle is too old to qualify for new car rates and used car rates are always higher, so you're likely to end up with a rate that's no better than what you have now, unless your credit substantially improved and you had a bad rate (for the time).

Navy Federal (Go Navy!) is my go-to. You can get 4.99% on a 3-year used car finance/re-finance now, so depending on what credit unions you can qualify for membership, you might be able to get close to that.

Here's a scenario: Let's say you financed about $35,000 for your Big Bend on a 5-year loan. You'll owe about $15,400 now, having paid about $5,300 in finance charges. If you keep the loan, you'll pay another $1,000 in interest by the time it's paid off in 2 years. If you refinance at 4.99% for 3 years, you'll pay $1,200 in interest and extend your loan one additional year. If your credit union will let you refinance for 2 years, you'll pay a little more than $800 in interest, so the refinance will save you a bit less than $200. For refinance rates that are higher, the savings drops. For example, 5.49% nets you less than $100 savings.

I was not offered that.Ford's ~60 months interest rates in December, 2021 were ~1.9-2.9% for qualified buyers.

.

I financed with Ford, got a $1500 rebate for doing so and then paid it off after the first month.I refinanced immediately after generating my first payment statement. Sent that first payment to Ford, then gave the loan to my Credit Union, and paid off the loan in the first year of ownership. The thought of making a car payment for 5 years...

What's the average car payment nowadays?

Me too. 1.9Hell no. I financed in 2021 @ 1.9%. I wouldn't go near today's rates. Plus note it'd be based on a higher (used car) rate.